One of the toughest aspects of being a top producing realtor is managing your time. Countless hours are spent focused in on your real estate business to ensure each client receives the level of service your sphere has come to expect when sending you a referral. But despite your meeting-filled calendar, your personal financial life still needs attention and can many times get neglected. As a result, building a financial team around you to partner with and delegate to when needed becomes a crucial decision.

There is a wide variety of service models you can choose from when selecting a financial advisor – and having options is always a good thing!

But with so many options to choose from, it is vital for top producers to align themselves with a financial advisor whose business has been designed especially for them. Real estate agents have a very unique set of financial circumstances, and by partnering with a financial advisor who is acutely aware of these factors, they can be served by a financial team that is fully equipped to take on their distinctive needs.

But how do you know if your advisor is a good fit for someone in the real estate industry? Well, if the advisor is proactively providing the following 11 services for you as part of their planning process, you are in the right spot.

Goal Setting & Accountability

For the same reason it is important that you set goals in your real estate business, it is important that you are setting goals in your personal finances. However, despite first appearances, your financial goals must be entirely separate from your business goals. It is true that the two lists are linked (after all, success in your business is typically the first domino to fall when we look at your ability to achieve your goals in your personal finances), but after putting together your list of personal financial goals, you will discover key differences.

Success in your business may be defined by certain levels of GCI, time off from work, or leads generated. While these are things that give you ammunition to reach your financial goals, you can’t stop at simply earning the income alone. You must deliberately make smart financial decisions with it.

The financial planning process is designed to first help you identify your unique financial goals, and second, to build out the steps you need to take in order to achieve them. Here are just a few examples of how you can apply your commission income toward actionable steps that will help you achieve your goals:

- Maxing out your Backdoor Roth IRA

- Maxing out your Solo 401k

- Maxing out your H.S.A.

- Contributing to a sinking fund to purchase a lake place in the future

- Contributing to your kids 529 college savings plans

- Paying the premium on your term life insurance

- Paying off any lingering consumer debt

The American Society of Training and Development (ASTD) has researched the concept of accountability and discovered the following data.

Success Rate for Completing a Goals:

- 10% – You have an idea of goal

- 25% – You consciously decide you will achieve the goal

- 40% – You decide when you will achieve the goal

- 50% – You plan how you accomplish the goal

- 65% – You commit to someone you will achieve the goal

- 95% – You make an accountability appointment with a person to whom you have committed

While your goals must ultimately be a personal decision, your financial planner should be doing two critical things to boost your probability of success: help you implement strategies today that will set you on the right financial trajectory, and act as your accountability partner for the long run.

Commission Income Management

One of the unique characteristics of a Top Producer’s financial life is the variability of commission income for which seasonality, real estate market cycle, and even commission splits play a role. Given this challenge, your financial advisor should be implementing a Cash Management Plan built out specifically for you. This is a plan that will combat your unequal income streams and allow you to maintain your lifestyle confidently through the ups and the downs of your business.

A good Cash Management Plan should be built on 5 different types of account types:

- Checking Account

- High Yield Savings Account

- Brokerage Account

- Retirement Account

- Illiquid Assets (such as investment properties)

Each of these accounts play a different role in your cash management plan and carry different risk and reward levels. While no account is more important than another, they all have their part in a balanced net worth.

Financial Plan Optimization

We believe that your financial plan is the intersection of your financial data and your personal goals. We also believe that financial planning is a process, and not an event.

Step one of any financial planning process should simply be getting yourself organized. You MUST gain clarity as to where you sit financially today before you can ever start planning for your future. Many people struggle to do this on their own, but it can be much easier with an experienced advisor who has a system for wrangling the data and creating a clear, concise summary of it.

Once you and your advisor have organized your financial life, regular planning check-ins to update both your changing data and your goals will be essential. And as your data and goals evolve over time, the correct financial decisions for your personal scenario will change, as well. Here are a few examples of questions that should to addressed and reviewed regularly during planning sessions:

- Cash management plan: Are accounts adequately funded for your goals?

- Rate of savings to investments: Does this need to increase or decrease based on goals?

- Percentage of net worth allocated to real estate: Are you overly concentrated to one asset class?

- Taxes: Are you taking advantage of all your options for tax savings both now and in the future?

- Life Insurance: Are you over or under insured for your stage of life?

- Investment allocation: Are you taking the appropriate amount of risk for your situation?

Again, the answers to these types of questions will most certainly change over time for the same individual. Accordingly, the job of a good financial advisor is to monitor your plan to verify each item is still in line with your overall goals and help you take advantage of opportunities as they present themselves.

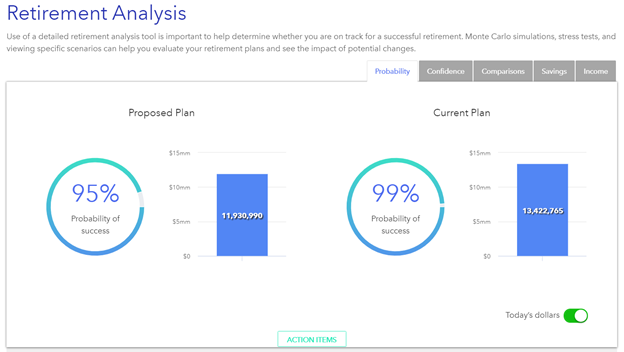

Retirement Planning

When do you want to retire? The answer can vary from “I love helping people find their dream home, I will never retire!” to “I just don’t have the energy to do all these showings anymore, get me out yesterday!” and everywhere in-between.

Regardless of where you may fall on that spectrum, having a plan that gives you the flexibility to retire on your terms makes you prepared for whatever changes come your way in life. There is a big difference in the mentality of agents who have grown their net worth to financial independence and continue to work because they love it, versus agents who continue to work because they have to.

There are many layers to piece together when it comes to solving the retirement planning puzzle. The list of confusing topics can include: Social Security, Medicare, rental income cash flow, RMDs, and systematic withdrawal plans. It can quickly get overwhelming. A good financial advisor will piece all of these components together into a financial plan tailored to your situation, with recommendations on how to navigate each.

Confidence is key when it comes to retirement planning, and financial advisors know that well. Therefore, a good advisor will not only be able to provide recommendations verbally, but be able to model “What if” scenarios for you, as well. Financial planning software can help you visualize exactly how certain factors can impact the plan over time. As a result, you’ll be able to make confident and informed decisions as your plan adjusts over time.

Tax Planning

The only two things that are certain in a financial plan are death and taxes! That’s how the saying goes, right? As a real estate agent, and inherently, a small business owner, you are likely very familiar with taxes, and you are accustomed to the cadence of your quarterly tax payments. While this is an excellent baseline, a good financial advisor will be able to help you make tax savvy decisions with your finances throughout the calendar year, instead of waiting until April 15th.

Here are a few tax planning considerations that your financial planner will help you figure out:

- Should your business be registered as an LLC or S Corp?

- Is the best retirement saving vehicle a SEP IRA or Solo 401k?

- Is it a good idea to hire your kids to help you with tasks for your business?

- Should you be contributing to an H.S.A. account?

- What are the tax implications of buying or selling an certain investment property?

Your financial advisor’s tax planning software should give you a good place to start in evaluating if a given tax strategy makes sense for your set of circumstances.

And remember, your financial planner typically isn’t your CPA, and shouldn’t pretend to be! The advisor’s job is to come along side your CPA as part of your financial team to help identify a potential strategy and get you the best outcome.

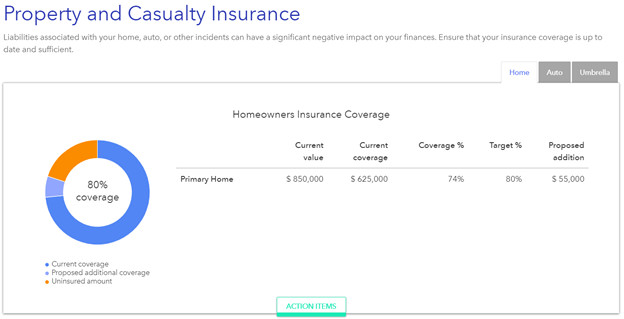

Insurance Analysis

Real estate agents are typically in need of insurance coverage that would otherwise come standard with a corporate benefits package; life Insurance, disability insurance, and health insurance to name a few. Due to the lack of built-in benefits with your chosen career path, reviewing your insurance policies becomes even more vital. Not to mention the P&C insurance that we all have to deal with!

While some financial advisors choose to become licensed to sell insurance products so they can handle insurance needs in-house, others have chosen to forego that option and remain “Fee Only”.

There is certainly a convenience factor to having your financial advisor be able to sell you the insurance you need, but it can also come with a conflict of interest when there is a commission involved for selling the product. The angle a “Fee Only” financial advisor would take in these circumstances would be to help you identify the need for insurance, and then bring in an expert in that field to implement the needed product.

Either way, your financial planner should be your go-to resource for determining how to navigate your insurance options and make sure that your risk has been sufficiently transferred when needed.

Rental Real Estate Modeling

Top Producers frequently accumulate an investment property or two over the course of their career, and in many cases, investment properties end up comprising a meaningful percentage of the agent’s net worth.

In these instances, it is vital that your financial advisor spends time planning for your biggest asset class – real estate – instead of spending the entire financial planning session discussing your investment portfolio. Especially if it only represents a much smaller piece of your net worth pie.

To clarify, a financial advisor’s job is not to be out searching for the perfect investment property for you; that’s your world. Where your planner should be stepping into your decision-making process is to help model exactly how your investment properties fit into your overall financial plan.

Some questions to tackle together might be:

- What impact does a positive or negative cash flow from an investment property have on my overall plan?

- How concentrated am I in real estate as an asset class and do more rentals make sense for me?

- What are the tax impacts of selling a property?

- Should we consider a 1031 exchange?

You bring the real estate knowledge. Then, combined with the financial planning experience of your advisor, you will be able to make confident decisions around not only your investment properties individually, but equally as important, how they will impact you financially for the long run.

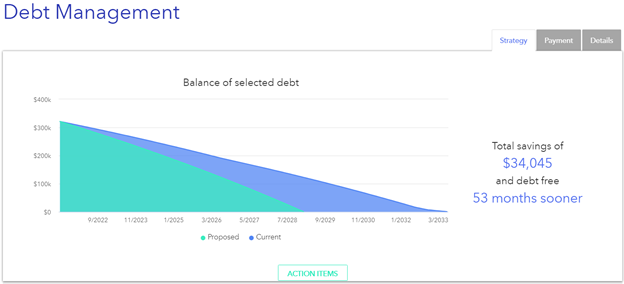

Debt & Mortgage Analysis

You likely have your ear close to the pulse of the interest rate market and are able to talk your clients through the basics before handing them off to a trusted loan officer. That said, we have found that sometimes the cobblers kids have no shoes. Meaning, you might know it is the perfect time to refinance one of your properties, but you just don’t get around to doing it. You’re too busy helping all of your clients!

That’s where your financial advisor should be stepping in and making that recommendation for you, as well as holding you accountable to maximizing your net worth by suggesting smart financial decisions that can otherwise slip through the cracks.

Ideally, your advisor might also be able to model how making certain tweaks – such as refinancing a mortgage – might impact your plan in the long run. After all, seeing the information represented in a visual way can make the options much clearer!

Estate Planning Review

Admittedly, estate planning isn’t the most exciting part of financial planning, but that doesn’t mean it isn’t extremely important. While your financial advisor is not your attorney and will not be drafting the documents needed to carry out a well-executed estate plan, he or she can be the quarterback of the process.

From the outset, the advisor can help initiate things by making sure the many layers of your net worth data are neatly organized in preparation for your estate planning meeting. This will help the attorney immensely in drafting the right plan for your wishes and for your assets.

Once the estate plan has been finalized, the advisor than also step in to help re-title or re-register certain assets, if needed. Your financial planner will be able to help you through this process, ensuring that nothing gets missed or skipped.

And don’t forget that life changes! Once you have your estate plan in place, you will want to review it periodically to make sure it still fits your wishes and assets accordingly.

Net Worth Concentration Review

One of the biggest risks we see routinely with Top Producers is an over concentration to real estate as an asset class. Now, step one in avoiding this is simply being aware of your net worth and what is it comprised of. In its most basic form, your net worth is the total of your assets minus your liabilities. Step two is determining what percentage of your total assets are invested in real estate.

As we mentioned earlier, it is not uncommon at all for agents to stumble upon a diamond-in-the-rough property and pick it up as an investment property. And that is a great thing! In fact, one of the biggest benefits of your career is leveraging your expertise to identify an inefficiency in the illiquid real estate market and profit from it.

Where it can potentially become a problem, however, is when you end up with all of your eggs in one basket.

Consider the tech bubble in 2001. We have all heard the horror stories of the folks who had their entire net worth wrapped up in company stock that went bankrupt. For the same reason it doesn’t make sense for tech employees to keep their entire net worth in tech stock, real estate agents should avoid building their entire net worth around real estate.

A good financial advisor will systematically review your net worth with you and be able to partner with you in determining the right amount of real estate for your specific situation.

Investment Portfolio Management

This component was very deliberately left to be last. The reason being, it should not be the sole value add of your relationship with your financial planner.

There is no denying that managing your investment portfolio is important, and your financial advisor needs to be great at it! That said, many times the advice stops with portfolio management when there is so much left to be done.

Once the plan components mentioned above are taken care of, though, it is critical to cover this meat-and-potatoes aspect of your plan in the home stretch of your planning process. Here are a few items around your investment portfolio that you should be addressing with your financial advisor:

- Is my asset allocation in line with my risk tolerance and time horizon?

- How do my portfolio expenses compare with the rest of the market?

- What is our process for decision making in a down market?

- Am I contributing to the right account types for my situation?

There are many more questions surrounding the topic of investment portfolio management, but those should get you off to a good start.

Having a strong relationship with your financial advisor can and should lead to a variety of conversations far beyond your investment portfolio. Furthermore, having a financial advisor that specializes in your specific situation allows you to leverage their expertise as compared to partnering with a generalist for your financial planning needs. And while your investment portfolio is an important part of your net worth, be sure not to neglect your other assets, such as investment properties, when building out your financial plan.