Does this scenario sound familiar to you? You find a client ready to move into their first home or dream home. They come to you in-hand with a pre-approval and you proceed to talk about what type of home they want and need. However, based on your MLS customized search, not much is available. And to make matters worse, the homes that are matching your clients search parameters are selling quickly and facing multiple offers (which may have increased the final winning sale price). So, you spend countless hours logging some serious windshield time showing more homes. The buyer seems to “like” the homes you’ve visited, but also point out things that they don’t like. Ultimately, the negatives outweigh the positives and you’re back to square one and the showings continue.

So how do you break this never-ending loop? Interest rates are low, buyers want to take advantage of the low rates, BUT there is a problem; there’s another housing shortage in your market. How do you combat this housing shortage issue?

One way to turn a housing shortage negative into a positive, educate yourself on renovation mortgage loans. Align with a reputable mortgage lender who’s certified in renovation lending AND has a proven process that protects the customer after the home loan closes.

Renovation Mortgage

How does a Renovation Mortgage combat the housing shortage problem?

Have you heard the phrase, “Work Smarter Not Harder”? Most likely you have. With a renovation loan, you can turn a like into a love! The customer can literally turn that outdated kitchen into the dream kitchen they’ve seen in magazines. They can update bathrooms, turn a one-stall detached garage into a two-stall attached garage, finish a basement, or even add a 2nd level to the home for added living space. With a renovation loan the realtor can cut down on the amount of homes they show a customer, and help the customer improve their equity situation (since the final loan to value is based on future appraised value with the completed renovations).

Let’s look at the different types of renovation loans

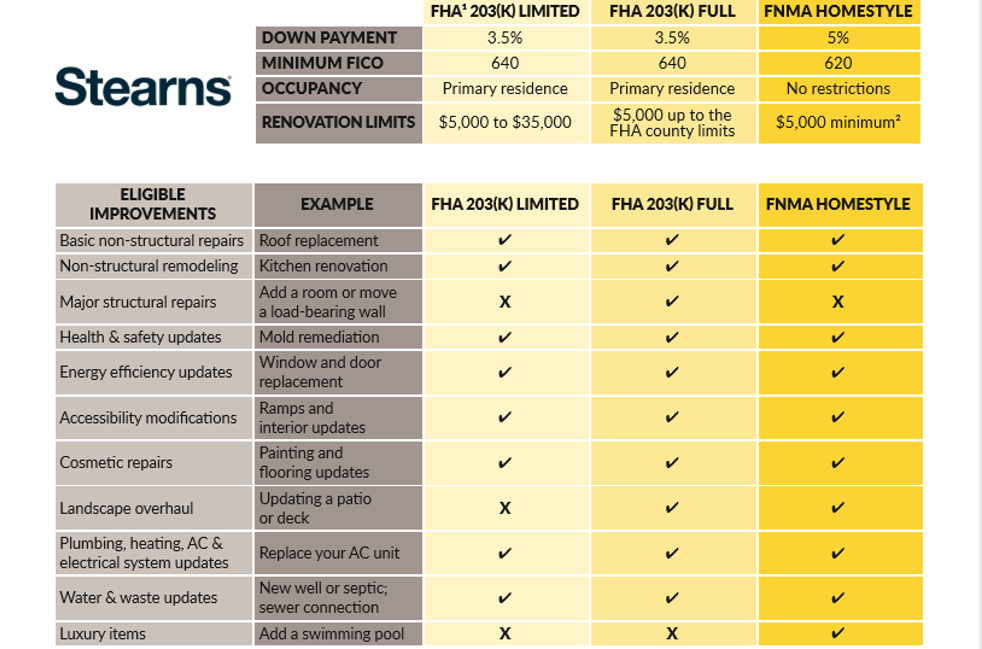

Fannie Mae Homestyle, FHA 203(K) Full, and FHA 203(K) Limited are the 3 most common types of renovations. See At-A-Glance. Some companies offer a specialized VA renovation product.

Do the Pros Outweigh the Cons?

Renovation loans can take longer to close, and are more complex on the surface, but they don’t have to be if you and your lending partner know what you’re doing. Typically, a renovation loan can take up to 45 days to close. That extra 15 days is necessary because the homebuyer must select a licensed contractor to do the renovations. Then the contractor must submit a detailed bid sheet to the lenders renovation coordinator for approval. The timing to receive this bid can be tricky, but since the lender must rely on this document to calculate the Total Acquisition Cost and Loan Amount, it must be finalized before they can even order the appraisal. This process protects the homeowner because a true renovation loan is a single-close loan. That means the borrower closes on the mortgage, then the total renovation costs get put into escrow and paid out to the contractor in draws after work milestones have been completed.

*One thing to note is the homebuyer cannot do the renovation themselves. A licensed contractor must go through a vetting process (which maybe different between every lender).

In closing, a renovation loan isn’t for everyone. However, it’s the type of loan that can open more doors for the new homeowner. The quality & condition of the home could even be considered distressed; and a renovation mortgage could turn that lump of coal into a beautiful diamond (aka dream home). So next time you’re looking at homes for a buyer, ask yourself if a renovation loan is right for this buyer. You could save them thousands of dollars and be a real hero!